The Free Application for Federal Student Aid

Helpful FAFSA Links

To apply for federal student aid, such as federal grants, work-study, and loans, you need to complete the Free Application for Federal Student Aid (FAFSA). Completing and submitting the FAFSA is free and easier than ever, and it gives you access to the largest source of financial aid to pay for college or career school.

In addition, many states and colleges use your FAFSA information to determine your eligibility for state and school aid, and some private financial aid providers may use your FAFSA information to determine whether you qualify for their aid.

In addition, many states and colleges use your FAFSA information to determine your eligibility for state and school aid, and some private financial aid providers may use your FAFSA information to determine whether you qualify for their aid.

FAFSA Facts

- The FAFSA is THE form required at all colleges that accept and award federal aid.

- It’s the form that provides your college financial aid officers with the information they need to go ahead and create your financial aid package.

- FAFSA stands for FREE Application for Federal Student Aid.

- Hence, it’s FREE.

- It’s available online at www.fafsa.ed.gov. NOT dot com, NOT dot org, NOT dot anything else.

- You can still get a paper version, if you really, really, really want to. But you don’t.

- It utilizes a July-to-June calendar. In other words, we are in the middle of the 2019-2020 year and seniors going to college in the Fall will apply for 2020-2021 aid.

- FAFSA opens October 1st every year. Some financial aid is first come, first served so it's best to complete it BEFORE November, but the state deadline is March 1st.

- The FAFSA helps determine the awarding of over $150 billion in federal aid, as well as state aid.

- The majority of colleges also use the FAFSA to determine who qualifies for their own institutional need-based aid.

- If you have your 1040 income tax return available, the form can be fairly straightforward.

- Do not pay someone to fill the form out for you to “maximize your aid potential”. Ms. Upton or any college financial aid office will help you for free.

- The FAFSA is based on your current household and your current assets. What you’ve got in the bank and investment accounts on the day you complete the FAFSA.

- But the FAFSA wants to know about last year’s (2018) income for your household.

- If your parents are divorced or separated, it’s based on the parent you spent the most time with in the previous year. And your step-parent, if there is one in that household.

- Don’t send notes to the federal processor. They’ll just shred ‘em. Your concerns and questions should be directed to the financial aid office of the school you attend or are planning to attend.

- Your parents saying that they won’t pay for College does NOT grant you independent status. To be considered independent, you have to be 24 years old, married, a military veteran or some other factors you can learn about here.

- If you have FAFSA questions, you can the federal government’s hotline at (800) 433-3243.

FAFSA Steps

Step 1: Apply for an FSA ID.

Apply for an FSA ID. Your ID will enable you to “sign” documents electronically, access your Student Aid Report (SAR) online and make corrections to your FAFSA through the web. Both the parent and student must each apply for an FSA ID , using separate email addresses. If you have applied for aid in past years, you can reuse your FSA ID.

Step 2: Submit the FAFSA.

You should file the Free Application for Federal Student Aid (FAFSA) as soon after October 1 as possible. The FAFSA is used by all colleges to determine your Expected Family Contribution (EFC) and your eligibility for federal and state aid, including subsidized student loans. Most colleges also use the FAFSA to determine your eligibility for institutional aid.

The FAFSA cannot be filed until after October 1st, but it must be completed and received prior to the college’s priority deadline date. The FAFSA must be filed for every year the student is in school. Submit your FAFSA online at fafsa.ed.gov. A FAFSA requires a signature from both a parent and the student applicant. To sign the online application, you must use your FSA ID (see Step 1).

There is no fee involved in filing the FAFSA and all families are encouraged to apply regardless of their family circumstances. Please reach out to Ms. Upton for assistance.

Step 3: Submit the CSS/PROFILE and other financial aid forms, if applicable.

Some private independent colleges require you to file a CSS/PROFILE application or an institutional financial aid form to determine your eligibility for their own sources of financial aid. The PROFILE application can be completed as early as October and is available here. Make sure you understand if you need to file any additional forms and that you submit them by the school’s specified deadline. A quick call to the financial aid office of your prospective school will let you know if there are additional forms to fill out.

Step 4: Apply for scholarships.

Millions of dollars in scholarships are available each year. Use tools like www.fastweb.com, myscholly.com, or goingmerry.com to search for national scholarships. Don't forget to check your guidance office and local library for more opportunities. Scholarships are a great way to help pay college tuition, books and living expenses and can reduce the amount you need to borrow. You should always maximize the amount of free money you use to pay for college before borrowing.

Keep in mind national scholarships are much more competitive and often times much harder to attain than local scholarships. Even though the awarded amounts on national scholarships may be higher, you most likely have a better chance of getting a scholarship from a local business or organization.

Step 5: Review your Student Aid Report.

After filing the FAFSA, you will receive a Student Aid Report (SAR). Correct any mistakes online by logging into your student aid account. Also add additional colleges where you would like your information to be sent.

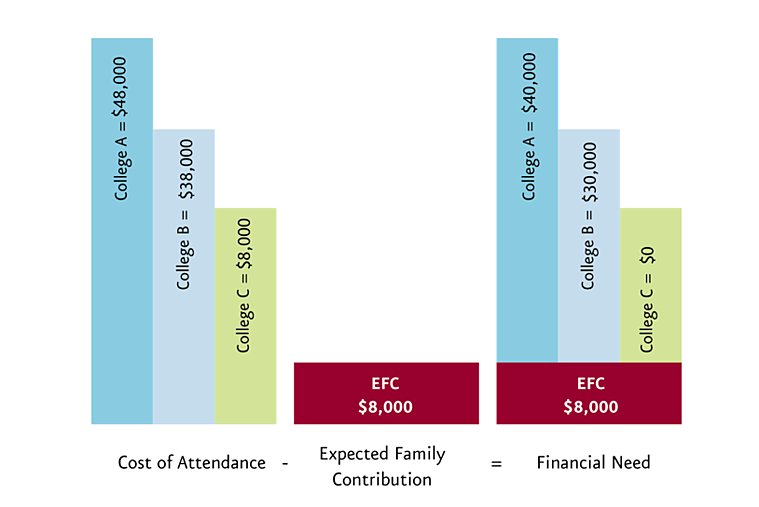

The EFC information from on your SAR will be sent to the financial aid office at the colleges that you indicated on your FAFSA form. Each college then takes that amount and subtracts the EFC from their total cost of attendance. That figure is your family's demonstrated financial need for that particular college. Financial need will be different for each college you apply to because each college's total cost of education is different.

Be sure to show your SAR to Ms. Upton so that she can look it over for any mistakes that could end up decreasing your aid amount!

Apply for an FSA ID. Your ID will enable you to “sign” documents electronically, access your Student Aid Report (SAR) online and make corrections to your FAFSA through the web. Both the parent and student must each apply for an FSA ID , using separate email addresses. If you have applied for aid in past years, you can reuse your FSA ID.

Step 2: Submit the FAFSA.

You should file the Free Application for Federal Student Aid (FAFSA) as soon after October 1 as possible. The FAFSA is used by all colleges to determine your Expected Family Contribution (EFC) and your eligibility for federal and state aid, including subsidized student loans. Most colleges also use the FAFSA to determine your eligibility for institutional aid.

The FAFSA cannot be filed until after October 1st, but it must be completed and received prior to the college’s priority deadline date. The FAFSA must be filed for every year the student is in school. Submit your FAFSA online at fafsa.ed.gov. A FAFSA requires a signature from both a parent and the student applicant. To sign the online application, you must use your FSA ID (see Step 1).

There is no fee involved in filing the FAFSA and all families are encouraged to apply regardless of their family circumstances. Please reach out to Ms. Upton for assistance.

Step 3: Submit the CSS/PROFILE and other financial aid forms, if applicable.

Some private independent colleges require you to file a CSS/PROFILE application or an institutional financial aid form to determine your eligibility for their own sources of financial aid. The PROFILE application can be completed as early as October and is available here. Make sure you understand if you need to file any additional forms and that you submit them by the school’s specified deadline. A quick call to the financial aid office of your prospective school will let you know if there are additional forms to fill out.

Step 4: Apply for scholarships.

Millions of dollars in scholarships are available each year. Use tools like www.fastweb.com, myscholly.com, or goingmerry.com to search for national scholarships. Don't forget to check your guidance office and local library for more opportunities. Scholarships are a great way to help pay college tuition, books and living expenses and can reduce the amount you need to borrow. You should always maximize the amount of free money you use to pay for college before borrowing.

Keep in mind national scholarships are much more competitive and often times much harder to attain than local scholarships. Even though the awarded amounts on national scholarships may be higher, you most likely have a better chance of getting a scholarship from a local business or organization.

Step 5: Review your Student Aid Report.

After filing the FAFSA, you will receive a Student Aid Report (SAR). Correct any mistakes online by logging into your student aid account. Also add additional colleges where you would like your information to be sent.

The EFC information from on your SAR will be sent to the financial aid office at the colleges that you indicated on your FAFSA form. Each college then takes that amount and subtracts the EFC from their total cost of attendance. That figure is your family's demonstrated financial need for that particular college. Financial need will be different for each college you apply to because each college's total cost of education is different.

Be sure to show your SAR to Ms. Upton so that she can look it over for any mistakes that could end up decreasing your aid amount!

Step 6: Compare your award letters.

Each college's financial aid office then determines what aid it has available to help meet your demonstrated financial need. Schools will aim to meet as much of your need as possible but not all schools can afford to meet 100% of your financial need. The financial aid office will put together a financial aid package or award letter for you. The aid may come in the form of grants, work study, scholarships, and student loans.

Remember, when your financial aid package arrives, read it over carefully. Decide if you want to accept any of or the entire award. Pay attention to instructions the school gives you. You may have to complete additional paperwork to fully accept the award. Accepting your award by the school’s specified deadline will safeguard it. However, if you feel that the award does not fully meet your financial needs or your needs have changed due to illness, unemployment or for some other reason, you can try appealing the award. Make sure to have documentation that supports your request. Many schools will take a second look at your package, if asked.

If you receive multiple financial aid packages, take note of which expenses are included in each school’s total cost of attendance when you compare. Also, pay attention to what kind of aid each school is offering your family. One school might meet a higher percentage of your need, but may do so with a greater proportion of loans. Sometimes, a school with a higher sticker price could end up costing your family less in the long run due to a better net price.

Your financial aid package may or may not cover your total financial need. If financial need is not entirely met, this unmet need is called a "gap." This means that resources must be found in order to meet the full cost of education. In many cases this will mean additional student and parent loans.

Ms. Upton can help you decipher your award letter and show you which college is offering you the best deal.

Step 7: Apply for loans, if necessary.

Your school may include federal student loans on your award letter. If these loans are not listed on your award letter, you still may be eligible to borrow. To accept your federal loan awards, you will need to complete a Master Promissory Note.

If you decide to take out a private student you will need to select a lender.